Would You Loan You Money?

Building A Bulletproof Credit Score

Welcome to the Scuttlebutt! If you aren’t subscribed, join the smart folks weekly in discussing business, finance, and self-improvement!

Last year, the credit score of the average American hit 711, an all-time high. Did we become better at managing our credit overnight or did something else change? The answer is maybe a little of both. In addition to the economy being pumped full of billions of stimulus dollars driving American savings rates also to all time highs, there were some changes made to how FICO, the credit rating agency Fair Isaac Corporation, interprets credit scores. While the bar for achieving good credit is continually moving, it is important to view raising your score as an opportunity to improve and improvement always starts with knowledge!

A personal note about credit

Everything in this issue is the information I’ve abided by to break a 790 credit score. I don’t bring this up to boast, I say it to show that a decent credit score is very attainable because I’ve done it. Understanding the requirements and taking it seriously is really all it takes.

I want to preface this issue with a few things. I cut my teeth on Dave Ramseys financial teachings which are vehemently against credit cards and credit as a whole. His teachings are fantastic, but I think he ignores people’s ability to change and has no faith in people overcoming a poor relationship with money. I think it is possible and important to handle rather than shy away from. Credit is a necessary evil that should be handled with absolute care - one wrong move and you can permanently impair your future.

Anyway.

Your credit score is not an arbitrary number assigned to you - it’s a direct reflection of your worthiness to handle money that isn’t yours. This is one of the biggest complaints I hear, that somehow they don’t deserve the number they have. It’s impossible for credit evaluators to know the ins and outs of your personal financial situation, but they do offer a breakdown of the 5 elements that make up your score.

Payment History

The first and most important item evaluated when looking at your history is “Does this person pay their debts on time”. This applies to not only your current credit card payments but also can extend into other areas like utility bills and rent if you’re not careful. Evaluators don’t care that you’ve paid your rent and utilities on time for ten years, they only care if you’ve missed payments. It seems unfair to only want the bad and not the good, but that’s the game.

A personal story

Taking care of your payment history is something that is near and dear to my heart. The first credit card I got when I was 18 (yeah I know, shocker), had a low limit and I was moderating it closely. At some point early on I moved, and I was still using mail billing as opposed to online payments. My credit card bill showed up to an old address and the bill ended up being sent to collections over a measly $200. That “hit” to my credit stayed on my report for 7 years. You can expect the same treatment with a simple mistake like this.

The best thing you can do for yourself when it comes to caring for your payment history is automate your bill pay. It takes just a few minutes to set up automatic payments for your rent, utilities, car payment etc. Not only does this guard the payment history section of your credit, but it also is one less thing you have to remember to do. Don’t give yourself the option to forget to pay. Automate automate automate.

Amounts Owed

Contrary to the title, amount owed isn’t about how much total debt you have. This large portion of your credit score is made up of what is called your “credit utilization ratio”. Credit utilization is the percent of the credit you use compared to what’s available.

An example

Let’s say you have one credit card with a limit of $1000. You buy a $500 TV with your credit card. At that moment, you are at a 50% utilization ratio, or using half of your available credit.

What’s important about this section in the eyes of creditors again goes back to your ability to pay. If you have a credit utilization ratio of 30%, you’re much more likely to be making your payments than someone with a utilization ratio of 90%. While there’s no specific number that is an “ideal” utilization ratio, it’s best practice to keep it under 30%. There’s an argument out there about maintaining 30% at all times, but that means continuously paying interest and I hate paying interest.

A few weeks back, I wrote an article about how to use Mint. There’s a great feature on Mint that shows you the utilization rate as a total and on each individual card you have. If you already have it set up and synced with your credit, click on “Credit Score” in the upper left-hand corner of the home page. Then click on “Credit Utilization”. Here you can keep a constant monitor of utilization on each card as well as overall.

One thing to note on credit utilization is your ability to manipulate this number. You can do this by contacting your credit card company and either raising or lowering your limits. Let’s say you can commit to spending $100 per month on your credit card and paying it off before it rolls to the next month. You get approved for a card but the starting limit is $1000. You can call the credit card company and have the lower limit to $300 which would make your $100 commitment close to that 30% ratio. The same can be done for increasing credit - I strongly recommend having a good understanding of your limits before taking the second option.

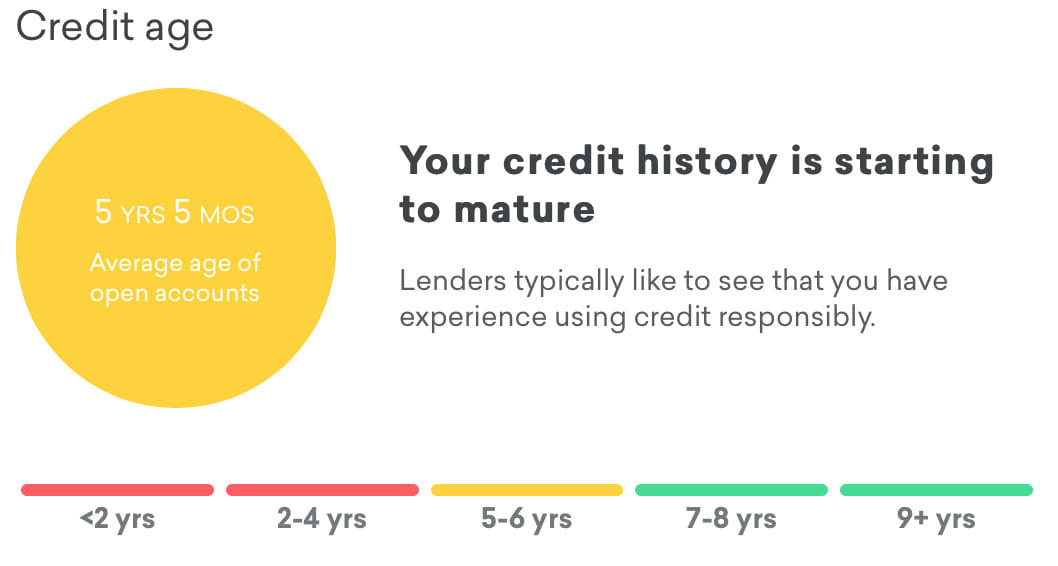

Length of Credit History

This one is pretty straight forward. Having a longer history of consistent payments looks good on your record, plain and simple. What tends to get people in this category though is closing credit cards.

Often times when people get on the warpath about paying off credit card debt, they commit to paying it all off and closing the card for good so they never have to worry about it again. There is something satisfying about that accomplishment, but in terms of your credit score, this is one of the worst things you can do. In this category, you want duration of credit. So that credit card you got when you’re 18 is contributing a lot of value to your total in this category.

The rating agency looks at all the different lines of credit you have and takes an average. The longer you have open lines of credit, the higher your average and score will be (for this category).

This explains why if you’ve ever seen your credit score drop after paying off a car loan or home mortgage. Car loans and mortgages are about 6 and 30 years respectively, which both are high on this time chart. Paying them off is a great thing, but unfortunately the way your score works, you will take a hit for it. I want to make a point here that you should NEVER not pay off your car or home for credit purposes. That’s silly. Pay the damn thing off, your credit will be fine.

Takeaway here is just because you pay off a card for good doesn’t mean close it. Cutting up the card and never using it again is better than closing the line together.

New Credit

New credit refers to the age of your credit like in the last category and also the amount of inquiries within a short period of time. If you walk into a department store and apply for a credit card, that inquiry for a new line of credit stays on your report for two years. Now the inquiry isn’t bad like say a missed payment. It’s just an inquiry. But let’s say 3 months later you apply for another new credit card, that’s when the red flags go up in the credit system.

It’s best practice to not open more than one new line of credit per 1-2 years if you can help it. Imagine you’re loan someone money and the next week they go to someone else to get another loan. Would that make you feel like you trust that person less or have a lesser likelihood to get paid back? Answer is probably yes. Credit card companies and institutions who make loans are the ones issuing money - don’t give them reasons not to trust you.

Credit Mix

The last element of your credit score is harder to quantify. There are two different types of credit that make up your “mix”; installment and revolving. Installment accounts are typically longer dated, fixed payment lines of credit like a car loan, home mortgage, or student loans. Revolving are credit cards and also home equity lines of credit. While they don’t say it explicitly, I believe that installment have a much larger impact in this category because they’re usually for bigger amounts.

Creditors want to see that you have multiple types of credit. While installment lines of credit are much more infrequent, it’s good to know the types and consider having a bit of both sides when trying to optimize your credit score.

Summary

Your credit score is an important piece of your financial life. Its this number that dictates what kind of terms you can get on loans; interest paid over the course of your life on any home loan, car loan, credit card, etc are all based on this number. Call it arbitrary or whatever you want - this is something you have to acknowledge and take care of.

Automate billpay so you’re never late

Keep total utilization rate low

Don’t close credit cards

Keep 1-2 years in between applying for a new card

Find a balance of long term and short term credit

I hope this information has been helpful. As always, my door/email are always open for help and questions at any time. I’ve put together a brief rating system below where you can rate the quality and content of this week. I strive to put out content that is helpful to you - any feedback you give helps me get better and you get more things you want to read. Please take a brief second and make a selection!

How would you rate this week’s issue?

Talk next week

~Brock

As someone who has gone from a 500 Credit score to now a 720 credit score these are amazing tips, and information. the sooner people learn this stuff the sooner they can start moving the needle in the right direction. Great article Brock.