The Joint ($JYNT)

Bringing Quality, Convenient, Affordable Chiropractic Care To Retail

If you’re not smart AND rich, you should be reading Scuttlebutt weekly. Drop your email below and we’ll get you there.

Good morning and happy belated 4th of July!

Today I’m going to cover one of my better investment ideas currently. In full disclosure, I own this company and plan to continue to hold it. This isn’t an offer or solicitation to buy or sell any security and is for informational purposes only. Please conduct your own due diligence and contact a financial advisor for guidance.

The Joint ($JYNT)

Market Capitalization: 1.2 billion

Last Twelve Months Revenue: 61.69 million

About

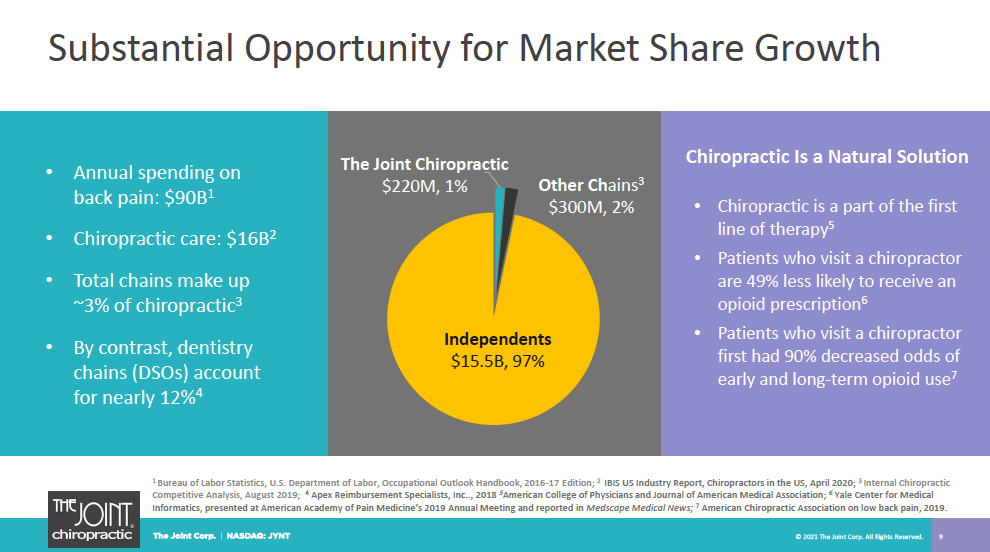

The Joint (JYNT) is a franchise model chiropractic clinic chain that offers adjustments strictly for private pay, cash, and non-insurance payments. The convenience of paying cash, affordability, and time commitment required compared to the alternatives make the Joint incredibly competitive in the chiropractic space. The average cost of an adjustment at the Joint is just $29 dollars whereas the industry average is $60.

Chiropractic Market

If you’ve ever experienced some form of back pain, you’re not alone.

“According to the American Chiropractic Association, 80% of Americans experience back pain at least once in their lifetime. According to the same 2018 Gallup report commissioned by the Palmer College of Chiropractic, eight in 10 adults in the United States (80%) prefer to see a health care professional who is an expert in spine-related conditions for neck or back pain care instead of a general medicine professional who treats a variety of conditions (15%).”

The Joint cites the IBIS World Chiropractors Market Research from 2020 stating that $16 billion dollars are spent on chiropractic services in the US every year. The total market is divided amongst what is mostly sole practitioners which leads to an extremely fragmented market. It’s estimated that the top four largest companies offering chiropractic services would each generate less than 1% of the total which leaves an opportunity for consolidation.

Customers

When it comes to customers, the market is just about, well everyone. Regardless of whether you work in a physical labor job or sit at a desk, chiropractic adjustments can be used to treat pain and as a preventative measure.

In 2020, the Joint performed 8.3 million adjustments to 1.1 million unique patients. Serving just over a million unique patients in a year on a base of about 210 million adults in the US shows the company is serving less than half a percent of the US population. It also indicates that the average patient is receiving 7.5 adjustments per year. As Joint continues to market its services to a population that is increasingly focusing on wellness and traditional remedies, I expect average adjustments as well as total unique customers to increase.

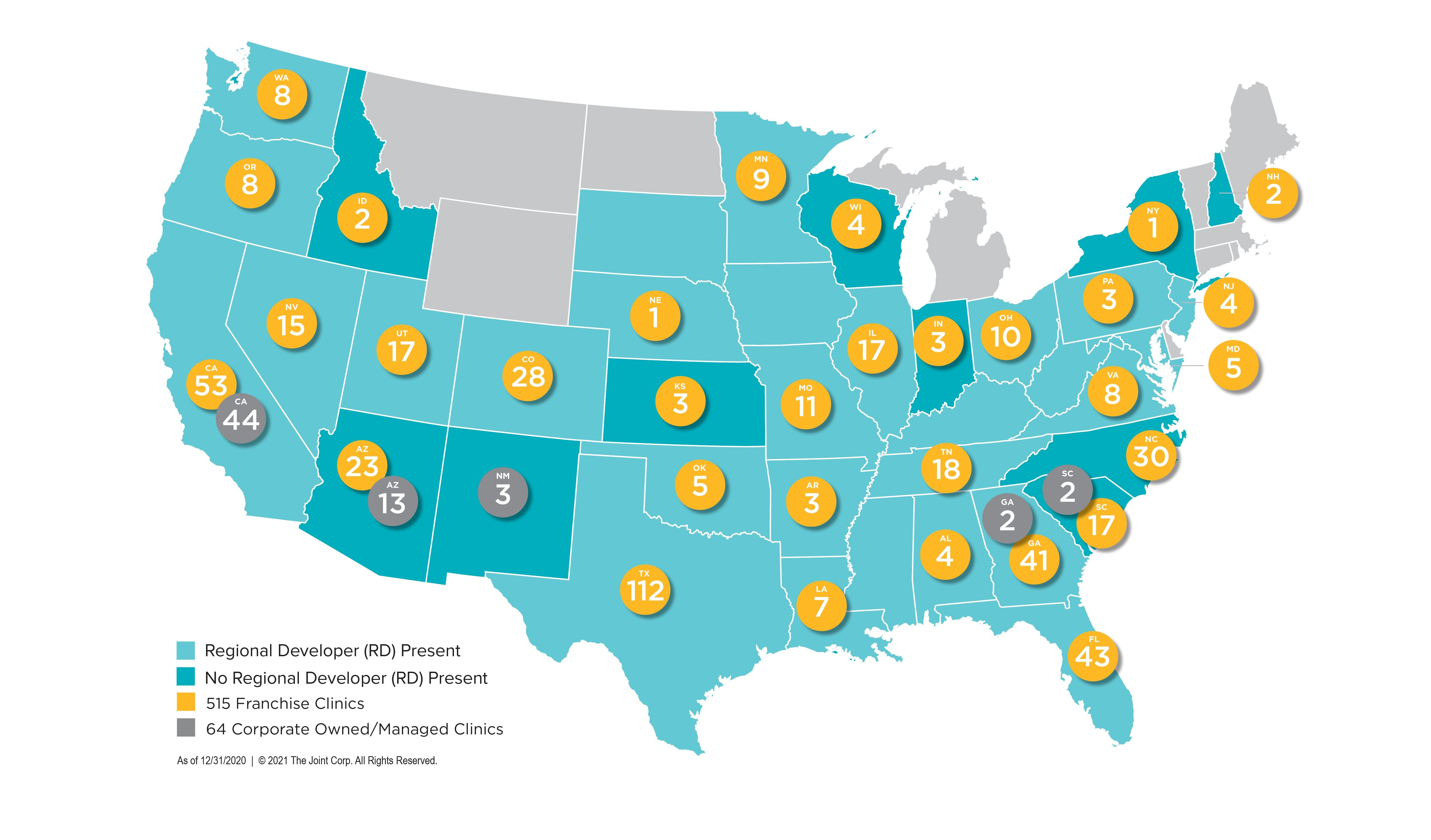

The following map’s orange indicators represent how many clinics are in each respective state. There is clearly lots of opportunity for states with no clinics and high population states like the Northeast.

What makes Joint unique in the chiropractic market isn’t better doctors or even the ability to take cash (most practices already do this but lean heavily on insurance options because that is primarily what people are used to). Joint’s value proposition is found in bypassing the tangles of insurance and offering a preventative as well as immediate care alternative allowing the consumer to continue to lead an active lifestyle. This creates a brand centered around wellness in an unbranded market.

Go to Market

The Joint is delivering chiropractic services to the market both through selling franchise licenses as well as operating wholly-owned locations. At of the end of quarter one, Joint had 592 clinics, 65 of which are wholly owned or “greenfields”. The company is looking to open 80 to 100 franchised clinics and an additional 20 to 30 greenfield locations by the end of the year.

The rate at which Joint is opening clinics is quite impressive. The company began with only 8 clinics open in 2010. Last year, despite COVID, was able to open 66 new clinics. Clinic growth is absolutely key to Joint’s growth strategy.

Management believes the US is able to handle 1800 total clinics. While this does imply a terminal saturation point, the company could open another 100 clinics per year for the next 12 years before hitting that point which is a lot of room for growth. This doesn’t touch on the company’s international opportunity which management has cited as something they are interested in pursuing.

Its clear management is eager to accelerate that growth towards 1800. The company has publicly set a goal for 1000 clinics to open by the end of 2023. If 100 new clinics are opened this year, that means the next two years must average 150. While this goal may be aggressive, I think it’s within reach.

Franchisees

When it comes to selling more franchises, the Joint doesn’t appear to have had any issues drumming up interest. Because of the low overhead requirements, the Joint cites startup costs anywhere from 200 to 400 thousand dollars to open a clinic. This is extremely low and opens the pool of available chiropractors and entrepreneurs to a wide audience.

Low startup cost also implies a quick payback period. The following chart depicts the breakdown for average initial cost, year sales based on same-store sales numbers, and time to break even. Based on this slide from the investor deck, most franchises have an expected payback period of around 3.5 years.

Location, Location, Location

The following map is a US geographic map of where the Joint believes the best possible clusters of concentrated customers exist. Knowledge of consumer demand coupled with high concentration areas allows Joint to focus its expansion of greenfield clinics in those areas to drive growth. Last month, Joint announced a clinic opening in Michigan as well as a planned series of 6 new clinics in Virginia.

The knowledge of the business also allows management to opportunistically buy back franchises or portfolios of franchises that can immediately drop revenue to the bottom line. Back in April of this year, bought two franchises in the Phoenix market along with 6 in a North Carolina market. Because of the nature of the business, little to no changes are required in the day-to-day operation of the business making the buyout immediately accretive.

How Money Is Made

The Joint makes money through six different channels: Greenfield clinics, royalties, advertising, software, franchise fees, and regional developer.

• Greenfield Clinics: The Joint recognizes revenue from the 65 owned clinics.

• Royalties: The company collects 7% of gross sales from each clinic.

• Advertising: Collects 2% of gross for advertising expenses.

• Software: The company charges a $599 monthly fee from each franchisor for use of proprietary chiropractic software.

• Fees: Purchasing a franchise costs a nonrefundable fee of $39,000 (dropped by 10k after first) - an initial term of ten years. There is no financing available for this option.

• Regional Developer: The Joint receives a fee from regional developers for exclusive authority to develop new locations

The following chart depicts a breakdown of revenue from 2019 to 2020 over the aforementioned categories.

The beauty of Joint’s pricing model is that it makes taking care of your back extremely affordable and convenient. The price of a single adjustment is $39 dollars, a package of multiple adjustments ranging from $21 to $33 dollars, and a monthly membership including multiple adjustments ranging from $17 to $20. In the investor presentation deck, The company cites that 85% of revenue comes from memberships. Recurring revenue gives great visibility into future revenue.

Another interesting note is the large portion of the revenue generated from greenfield clinics. In 2020, Joint operated 64 greenfield clinics. This means that 11% of the total clinics accounted for 52.3% of revenue last year. Seeing these numbers makes it clear why management is focusing on driving the wholly-owned segment of growth.

The last thing I find particularly great about the business is the speed at which chiropractors are able to service customers. Joint states that brand new customers can come in and leave with an adjustment in under 20 minutes while an existing customer can leave in an average of 7 minutes. With low fixed costs and virtually no variable cost, the more patients that can be adjusted the better. Low time requirements allow big opportunities to serve a lot of patients. This is seen in the growing gross margin over time.

Higher margins mean more revenue dollars falling to the bottom line.

Financials

A major criticism of Joint has been the slowing revenue growth as seen in the prior snapshot. While it has been decelerating, I believe we should expect to see mid-twenty percent revenue growth consistently going forward.

COVID didn’t put a huge damper on the business last year but I don’t think it allowed the company to grow at the rate that it could have without it. The company’s goal of 1000 clinics at the end of 2023 implies growing total clinics by 66% over the next 2.5 years. If executed on, revenue growth should hover in the mid to high 20% range.

Joint is currently in a strong financial position with 17 million in cash and no long-term debt.

Although I don’t think valuation is the most important thing when it comes to finding good businesses, it’s important to mention where Joint sits currently. Joint is not cheap by about any metric. At a 1.2 billion dollar market cap, Joint trades for 19x sales, 18x EV/Rev, and 118x EV/EBITDA (all LTM - not big on forward projections and like to see at what the company has executed on thus far). A recent announcement that the company will be joining the S&P Small Cap 600 has driven the price up materially, but I believe there’s still a lot of runway in this business.

Management

One last thing I always like to look at is who is running this business and what kinds of incentives they have. The CEO, Peter Holt, has a long history involved with franchises including operating and turning a business into a franchise model.

Here’s a screenshot from the company’s proxy statement.

The fact that the company believes it is important the directors and executives need to hold stock in the company is a great example of aligning incentives. Holt actually holds close to 20 million dollars in company stock at this time. I love some skin in the game when it comes to finding great companies.

Conclusions

While I don’t think Joint is a 100 billion dollar business, I think it’s extremely plausible its a 10 billion dollar business in the next ten years. The franchise model is extremely powerful when operated correctly - see Dominos pizza, Planet Fitness, or Winamark. It’s difficult to make direct comparisons for Joint because there’s nothing exactly like it, but those are three examples of businesses leveraging the franchise model correctly.

At the end of last quarter, CEO Peter Holt said the following:

“We continue to strive toward our goal of 1,000 open clinics by the end of 2023, which we expect to be a tipping point. At scale of this magnitude, as proven repeatedly by many franchise systems that are now household names, we can more easily and effectively leverage our brand, marketing and operations foundation, which we expect to drive growth at an even faster pace. Combined with the large and expanding chiropractic care market opportunity, we believe in our long-term ability to increase stakeholder value.”

Focus on leveraging scale within the franchise model as well as operating greenfield clinics effectively will be the keys to Joint achieving that kind of valuation. As I said before, I own a material position in Joint and will continue to hold as management consolidates share of the chiropractic market.

I hope you found this analysis interesting and informative. As always, I would love your thoughts, questions, critiques, and feedback. You can do that by replying to this email, commenting on the post, or hit me up on Twitter (@brockhbriggs).

Talk next week,

~Brock